The CRB index has recently broken below its 15-month support zone between 176 - 179, which had held since April 2016.

We have seen weakness in the gold price over the past two weeks, and if gold fails to break higher from its ongoing consolidation over the next 3-6 months, a significant culprit will selling among broad-based commodity funds. Below we zoom in on a detail of the CRB Commodity Index, which gold measures an average price level of 19 commodities including gold, silver, platinum, palladium, the industrial metals, the energy complex, and agricultural products.

Note that the CRB index has recently broken below its 15-month support zone between 176 – 179, which had held since April 2016.

Image A

Our technical target for the CRB over the short run is 158 on the index – in other words, a retest of the 2016 lows. This target is calculated by subtracting the amplitude of the failed advance above the support zone (19) from the breakdown point (177). Fundamentally, it represents an equal number of long contract holders who are likely to liquidate below the breakdown point as who bought above the support zone over the past year.

Gold Sometimes Grouped with Other Commodities

Although gold is certainly not simply another commodity like the rest of the CRB index, during times in which investor psychology is preoccupied with “hot” markets such as technology stocks (Amazon, Facebook, etc.), real estate, and crypto-currencies, sentiment tends to fade against all commodities.

We might disagree with the market fundamentally, i.e. we know currency debasement and unsustainable debt continues to increase every day, but a key point of our philosophy is to put our own fundamental opinion second, and to respect the market first.

At present, the market is seeing less of a need for safety due to a focus on hot risky asset classes, and so that component of gold demand is absent. We are thus witnessing gold and silver have a high correlation with the rest of the commodity complex. In such an environment, when institutional funds place sells orders for their diversified commodity holdings, gold is dumped in tandem with the group.

Yes, gold has been outpacing the rest of the commodity complex since the late 2015 lows. However, such relative strength is not always sufficient to stop precious metals from falling in a general commodity liquidation over the short run.

If we see gold break down below $1,230, a key short-term support level, a continued decline in the CRB index will be a major contributing factor.

Commodity Index Long-Term

Below we back out the chart for the CRB index from 1974 – 2017:

Image B

It should be noted that broad commodities are now the cheapest they have been in 43 years nominally, and by far the cheapest in real terms (adjusted for inflation).

The low of 2016 is in the process of being retested, which is what may lead to near-term weakness in gold – but in viewing the chart above we must seriously ask the question: how much lower can commodities fall from 43-year lows?

These are tangible materials of finite supply in the earth’s crust, which the ever-growing world population consumes every day – a reality that will not change in our lifetimes unless technology to harvest minerals from asteroids arrives soon, a scenario still the realm of science fiction works.

The CRB Commodity Index cannot go to zero as a currency or individual stock can, yet this is the lowest that commodities have been in four decades. When things that cannot go to zero are priced at their lowest in over a generation, we must view the relative risk/reward proposition as favorable from a long-term perspective.

Our assessment is that even if moderate weakness continues for several months to 1-2 years, broad commodities are much closer to a long-term bottom than a top.

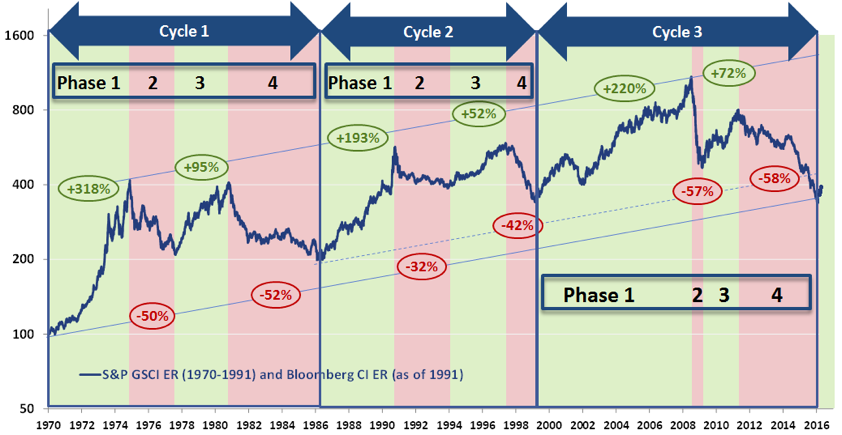

Image C

Commodities are cyclical in nature. The chart at right shows the three major cycles that the commodity complex has seen since the 1970’s, divided into two sub-phases each of boom and bust cycles (green and red shading, respectively).

Booms and busts are an inherent feature of the typical 10-20 year delay that it takes for the mining lifecycle to move from:

- (a) mineral discovery through

- (b) mine permitting to

- (c) construction to

- (d) successful production which then

- (e) increases supply in the market.

It is said that in commodities “low prices are the solution for low prices”, as marginal mine supply is eliminated when prices fall, eventually forcing prices higher again. We are seeing this phenomenon already in many junior oil and precious metals companies: deposits which were once economic are no longer at today’s low commodity prices, and thus the mines are placed on care and maintenance, reducing supply until higher prices emerge.

Takeaway on Commodities in Relation to Gold

Even if weakness continues in the commodity complex through the remainder of this year, our assessment is that most commodities are much closer to long-term bottoms than long-term tops. Of course, each commodity will move at different times and with a different set of fundamentals. Yet the macro analysis shows a world preoccupied at the moment with the bull markets in digital technology – but as day must follow night, higher commodity prices must follow a period of lower prices. Gold selling due to broad commodity weakness is thus limited in the big picture, even if weakness over the short run cannot be ruled out.

Christopher Aaron,

Bullion Exchanges Market Analyst

Christopher Aaron has been trading in the commodity and financial markets since the early 2000's. He began his career as an intelligence analyst for the Central Intelligence Agency, where he specialized in the creation and interpretation of the pattern of life mapping in Afghanistan and Iraq.

Technical analysis shares many similarities with mapping: both are based on the observations of repeating and imbedded patterns in human nature.

His strategy of blending behavioral and technical analysis has helped him and his clients to identify both long-term market cycles and short-term opportunities for profit.

Share: