The Federal Reserve meeting last week resulted in no change to the US central bank's short-term interest rate target, and weighted down a gold price.

Gold price fell $41 from a week prior to close at $1,227 as of the final trade on the New York COMEX on Friday afternoon. This represents a 3.3% drop from the close a week prior.

A bounce is due, but we clearly see that the gold market wishes to consolidate further over the short-run.

Image A

The importance of the pennant consolidation breakout that must necessarily occur by Q3 – Q4 is not lessened by the consolidation that is underway – in fact, it is only strengthened in its eventual resolution. The more time that gold remains within the context of the consolidation defined by the falling long-term downtrend (magenta color) and the rising blue support, the stronger the breakout that will happen when this pattern is resolved.

Short-term traders are cautioned that volatility and thus opportunity for profit should subside as the consolidation progresses this summer and into Q3. The definition of a converging pennant consolidation is volatility that lessens as buyers and sellers each exhaust one another. The pending new market trend occurs because the next influx of large buyers or sellers is met by exhausted existing participants.

The boundaries of gold’s consolidation now come in at:

Upper boundary: $1,290 and falling.

Lower boundary: $1,155 and rising.

Again, over the short-run, we anticipate gold is due for a bounce, likely back to the $1,240 - $1,260 region, before consolidation continues through this summer, the technical action for which will be less meaningful within the above ranges until Q3. Our 12-month target upon a breakout remains significantly above or below the $1,205 apex of the consolidation – $1,535 or $875 – dependent on the direction of the breakout. This target is derived from taking widest amplitude ($330) of the converging consolidation and adding it to the apex of the pattern.

Fed Meeting

The Federal Reserve meeting last week resulted in no change to the US central bank’s short-term interest rate target. The Fed funds rate remains at generationally-low levels, at a range of 0.75% - 1.00%.

The language accompanying the Fed non-decision is being closely securitized by the market:

"The Committee views the slowing in growth during the first quarter as likely to be transitory and continues to expect that, with gradual adjustments in the stance of monetary policy, economic activity will expand at a moderate pace, labor market conditions will strengthen somewhat further, and inflation will stabilize around 2 percent over the medium term.”

Translated from Fed-speak, this moderately-positive outlook suggests that the Fed will look to raise interest rates at its next meeting, on June 14.

We remind new readers that – contrary to the faulty-logic repeated in most mainstream media outlets – rising interest rates have most closely corresponded with rising precious metals prices throughout history.

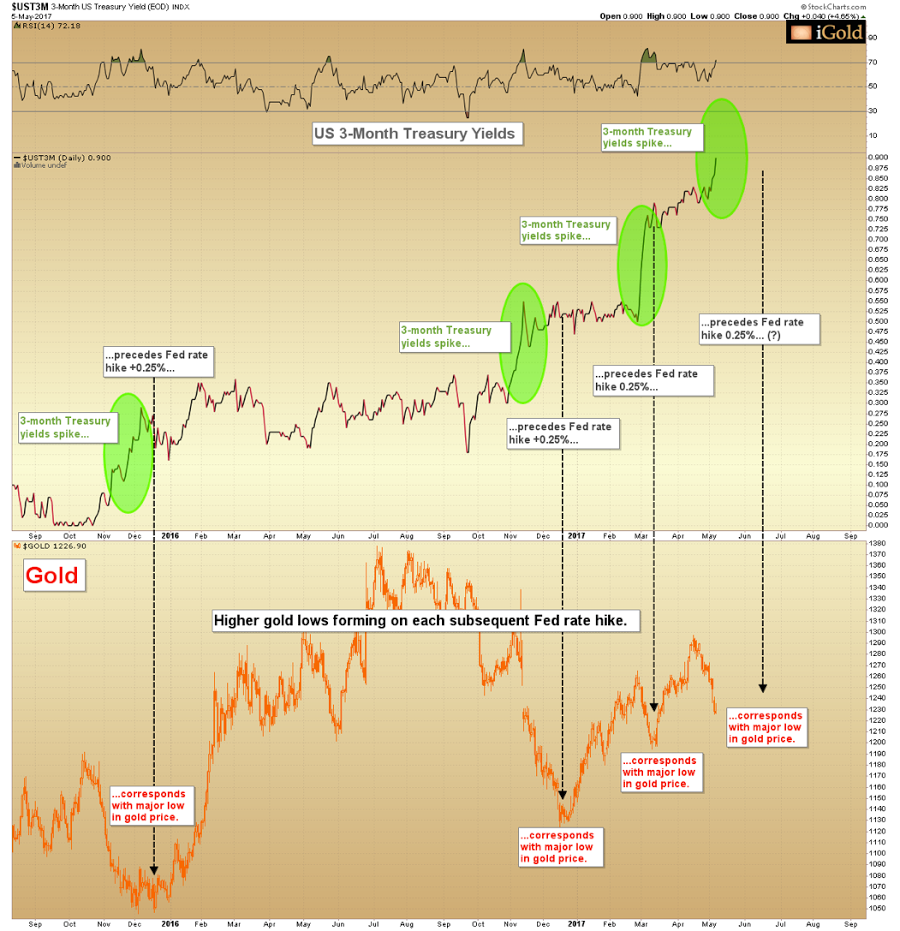

Indeed, since the first interest rate hike in almost a decade in December

2015, each of the following hikes have been met by higher lows forming in the gold price:

Image B

First Fed rate hike – December 2015 – gold: $1,045.

Second Fed rate hike – December 2016 – gold: $1,122.

Third Fed rate hike – March 2017 – gold: $1,198.

Our own proprietary technical model, which relies on 3-month Treasury yields as a leading indicator, indeed suggests that a fourth Fed rate hike is pending. At right we show the 3-month yields on top, with the price of gold immediately below, since 2015. Note how US 3-month yields have spiked several weeks in advance of each of the first three rate hikes. Essentially the Fed is responding in policy to higher yields in the short-term Treasury market.

The important point is that the rate announcements have almost exactly corresponded with major lows in the price of gold.

Gold Traders Have Been Wrong Three Times…

At some point, we should expect gold futures traders – who have gotten this trade wrong on each of the prior three Fed rate hikes by selling in anticipation of the rate increase (only to see gold rise strongly against them after the announcement) – will wake up and cease this losing strategy. Thus, likely this year, gold may be expected to form its next intermediate low weeks in advance of the Fed announcement as traders wise up.

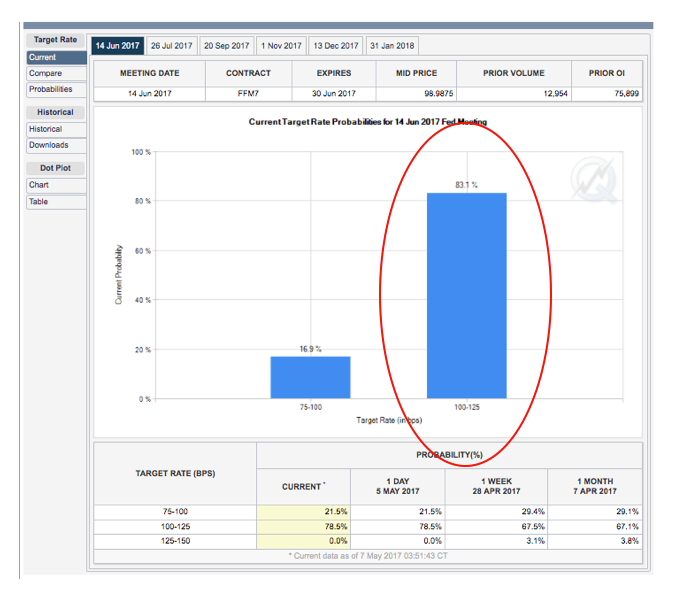

The futures market is also pricing in a fourth rate hike, as can be seen below by the 83.1% odds that traders are assigning to the pending outcome:

Image C

Any gold price low above $1,198 on a fourth Fed rate hike would thus keep the trend of higher lows intact on the first four rate hikes since 2007. In a market that may be commencing a period of several years of additional Fed hikes, this trend bears continual monitoring.

Christopher Aaron,

Bullion Exchanges Market Analyst

Christopher Aaron has been trading in the commodity and financial markets since the early 2000's. He began his career as an intelligence analyst for the Central Intelligence Agency, where he specialized in the creation and interpretation of the pattern of life mapping in Afghanistan and Iraq.

Technical analysis shares many similarities with mapping: both are based on the observations of repeating and imbedded patterns in human nature.

His strategy of blending behavioral and technical analysis has helped him and his clients to identify both long-term market cycles and short-term opportunities for profit.

Share: