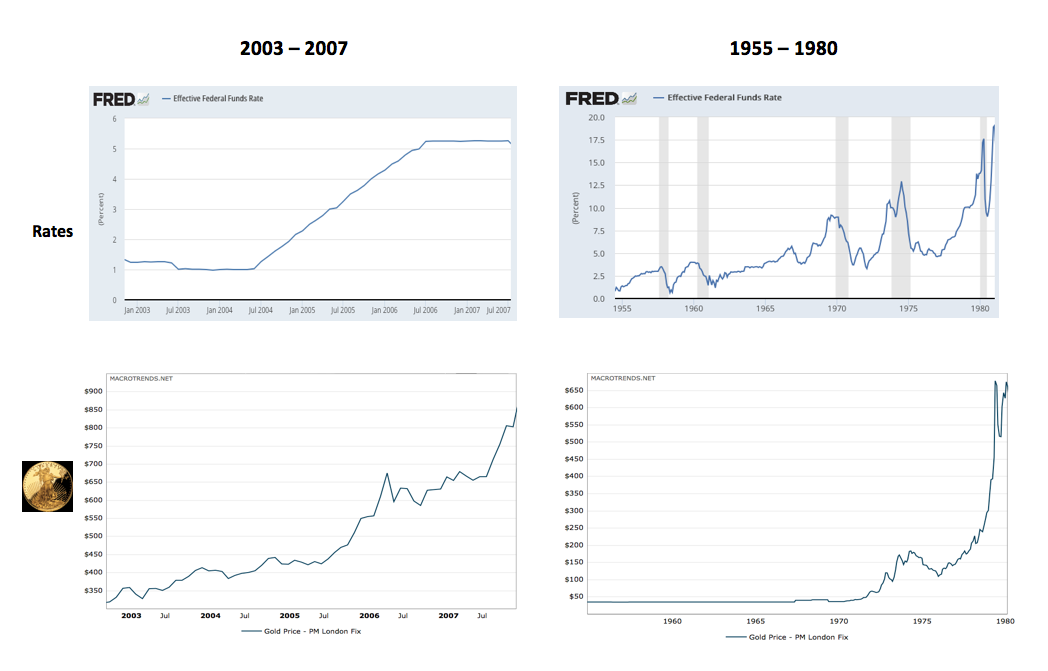

I've long stated that the mainstream media consistently gets the relationship between gold prices and short-term US interest rates wrong. The charts clearly show over both recent and historical cycles, rising interest rates have corresponded with rising gold prices - not the opposite, as erroneously stated by the majority of the press.

For example, we’ve shown in the past the following two data sets: gold prices and short-term rates from both 2003 – 2007, and 1955 – 1980:

Image A

In this case, the data as presented in the historic charts is extremely clear. And while we are officially told by the financial industry that “past performance is no guarantee of future results” when discussing historical trends, to completely disregard lessons from the past would be akin to saying “past train arrival times are no guarantee of future train arrival times” or “past dinner prices are no guarantee of future dinner prices.”

Sure, we cannot know everything about the future from studying the past. Things do change.

But we can know something.

And is not knowing something about what to expect in a given market better than not knowing anything?

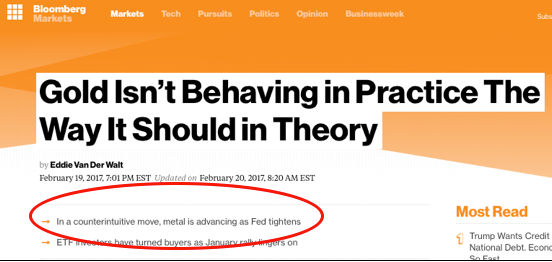

In this light, I continue to be amused and dismayed when I see articles such as this Bloomberg piece every time gold begins to get any attention in the mainstream press (see highlight circle):

Image B

The article’s main point is that gold is behaving “counter-intuitively”, since it has risen after each of the Fed’s two interest rate hikes over the last year. The article goes on to state how rising interest rates are supposed to be positive for the dollar due to higher interest potential, and therefore negative for gold.

Does Bloomberg bother to look at the actual historic correlations between gold and short-term rates as we have shown above?

The main point of this editorial is to give an illustration of why I focus so heavily on charts and not on reported “fundamentals.” Many who believed the Fed would raise rates in 2015 for the first time in a decade stayed away from precious metals complex because they believed the fundamentals written in 99% of the mainstream financial press.

Even the respected economists all agreed on the fundamentals: rising rates are bad for gold.

The historic charts said otherwise.

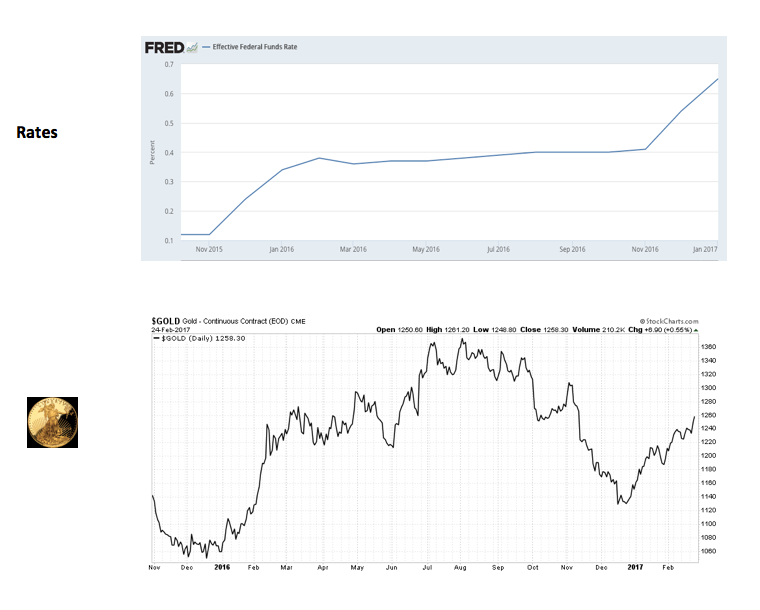

As we observe the current cycle underway since December 2015, which form of analysis has been more accurate thus far?

Image C

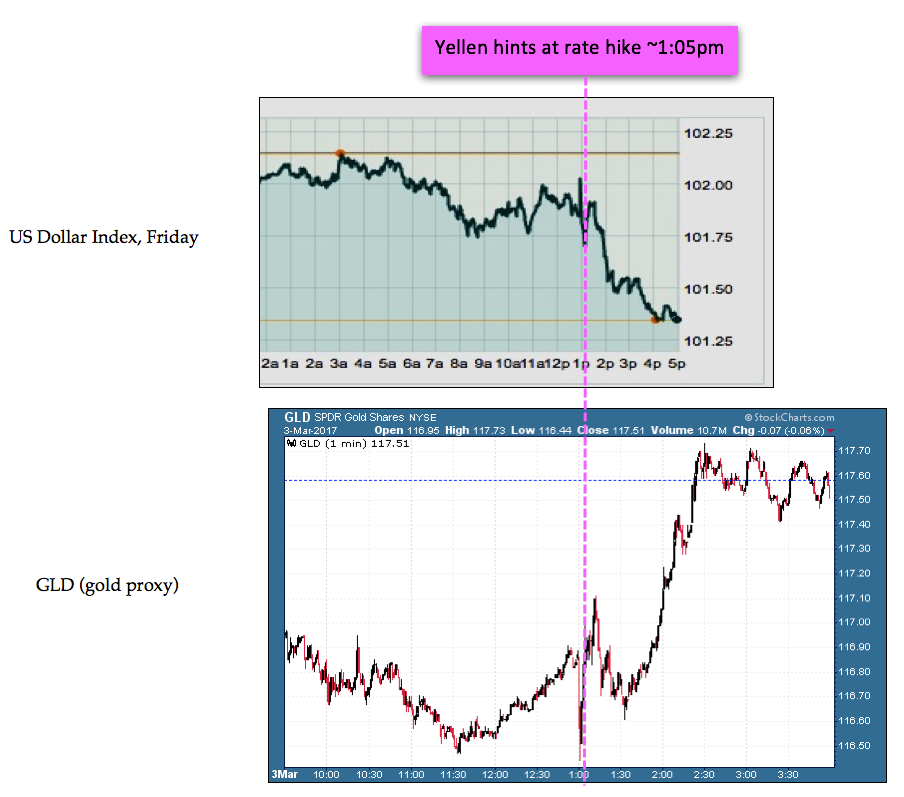

Fed Hints of Coming Third Hike

Friday was a fascinating case in point. Federal Reserve Chairwoman Janet Yellen gave a speech in Chicago Friday afternoon in which she strongly hinted that the US central bank would raise interest rates for the third time at this upcoming Fed policy meeting, scheduled for March 14-15. The most prescient quote from the speech follows:

“We currently judge that it will be appropriate to gradually increase the federal funds rate if the economic data continue to come in about as we expect. Indeed, at our meeting later this month, the committee will evaluate whether employment and inflation are continuing to evolve in line with our expectations, in which case a further adjustment of the federal funds rate would likely be appropriate”.

Again, the standard narrative presented in the media is this: an increase in Fed-controlled interest rates should be US dollar-positive, as, all else considered, investors would increasingly choose to hold reserves in the US currency as interest rates rise, since they would be able to achieve a higher yield on these short-term deposits. This is the standard explanation for why rising interest rates should cause the dollar to strengthen, and hence precious metals to fall.

So if the above narrative were true, why did we observe the following reactions in the foreign exchange and precious metals markets immediately following Yellen’s speech? Let us look closely at the charts of both the US dollar index and gold on Friday.

Image D

Notice that the US dollar fell after the hint of a rate hike, losing over 0.6% in just a few hours, while gold rose nearly $8 in the two hours after the speech. This is the exact opposite to the pattern of trading that we are supposed to see with reference to Fed policy and major currency markets. The US dollar is supposed to rise and gold is supposed to fall on interest rate hikes.

The mainstream media has it flat-out wrong. Friday was a small example of that. Neither the dollar nor gold have behaved the way they are supposed to since the first Fed rate hike in nearly a decade, 15 months ago. We continue to see dollar weakness and gold strength appearing every time either a hint of a rate hike surfaces, or an actual rate hike is announced.

Considering that rates finished a 35-year falling cycle from the 1980 peak in 2015 and could reasonably be expected to be on a rising trajectory for many years or decades, this relationship is of utmost importance to get right.

Will the trend continue on March 15 if another rate hike is announced? We will know soon.

Christopher Aaron,

Bullion Exchanges Market Analyst

Christopher Aaron has been trading in the commodity and financial markets since the early 2000’s. He began his career as an intelligence analyst for the Central Intelligence Agency, where he specialized in the creation and interpretation of pattern-of- life mapping in Afghanistan and Iraq.

Technical analysis shares many similarities with mapping: both are based on the observations of repeating and imbedded patterns in human nature.

His strategy of blending behavioral and technical analysis has helped him and his clients to identify both long-term market cycles and short-term opportunities for profit.

This article is provided as a third party analysis and does not necessarily matches views of Bullion Exchanges and should not be considered as financial advice in any way.

Share: